A fellow dentist recently posted in the Dentists Who Invest Facebook Group — they wanted to renovate their house and were torn how to fund it

They described their options as:

A) Pull they money out of an ISA (Their account had not really grown in value in 5 years)

or

B) Borrow against their property to fund a £60–70k renovation, with mortgage rates falling

And to be fair it’s a common dilemma

Should you cash in an investment that’s gone nowhere - or leverage your property while interest rates are still bearable?

They also mentioned in their post that their investment portfolio was "low risk" as this is what was deemed most suitable by their fund manager.

I had some thoughts as to what was REALLY going on - so I dropped a reply.

Here’s what I said:

"Hi there good q

Assuming the money is for long term retirement…

The reason why one gets attributed these low risk/low growth portfolios is due to risk profiling. The adviser is obligated to require a client to complete a risk profile questionnaire as part of their assessment.

If this risk profile is found to classify the potential client as risk adverse then they are usually paired with a “low risk” portfolio which has a high bonds allocation

Risk is usually equated to mean risk of losing our money (capital loss) however in this instance they are equating risk with volatility (price fluctuations) which is actually far from the same thing

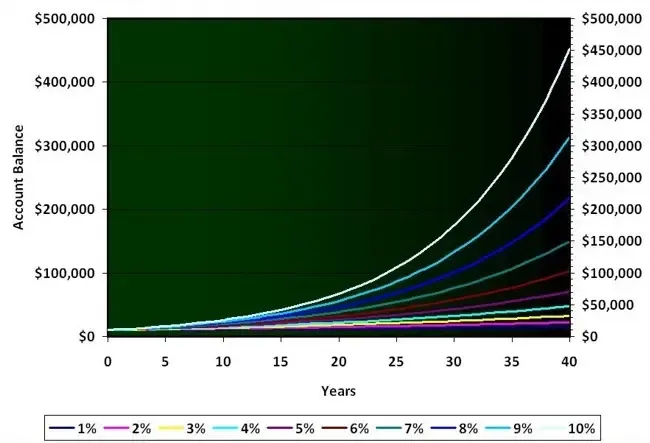

By seeking to dampen volatility overly so one can also massively dampen the potential returns of their investments. In the context of constant inflation (3-4% yearly) which is the greatest risk of all such a portfolio may not be able to provide any sort of real return and in fact potentially even lose money in real terms. (This is all while the portfolio manager is making money regardless from your investment fees)

A decent well returning portfolio would be able to outpace inflation and also likely mortgage interest rates/house prices. This can mean it makes more sense to allow the money to roll up in some sort of investment and not cash out

Two options here would be invest some time to learn how investing works or possibly seek advice from a professional if uncertain. Both defo worth it here

Hope that goes some way to assist 🙏🏻"

And so we now see how low or even medium risk portfolios are often inhibiting our returns and financial plans.

Not saying they aren't appropriate SOMETIMES - but if you ask me they are recommended far too often

So in short...

Most people are to a degree misallocated reduced risk portfolios due to outdated risk profiling methods

Risk ≠ volatility (a major myth)

Inflation’s quietly eating your cash while the managers of poor performing funds still get paid

And the real “risk”? It’s not being able to best inflation.

We talk about this kind of thing all the time inside the Dentists Who Invest Facebook Group. Feel free to join if that sounds like your thing

About how to make your money work smarter, how to spot dead weight investments, and how to build a financial plan that doesn’t rely on hope

Here's to your investing success

- Dr. James

Enter your details above to receive a link you can use to download your FREE pdf

Read More

Here's What New Associates Need To Know

What Is Your Definition Of Retirement?

How Often Do You Look Back On Your Life And Think “I Wish That I Knew Than What I Know Now?”

Can I Invest In My ISA For Passive Income?

The Role Of Luck In Investing

DENTISTS WHO INVEST LIMITED IS A LIMITED COMPANY, REGISTERED IN ENGLAND AND WALES