An interesting fact is that the majority of individuals’ retirement portfolios consist of some combination of bonds and stocks. These are known as paper assets, as originally they were recorded and traded on paper. Nowadays they are of course digital.

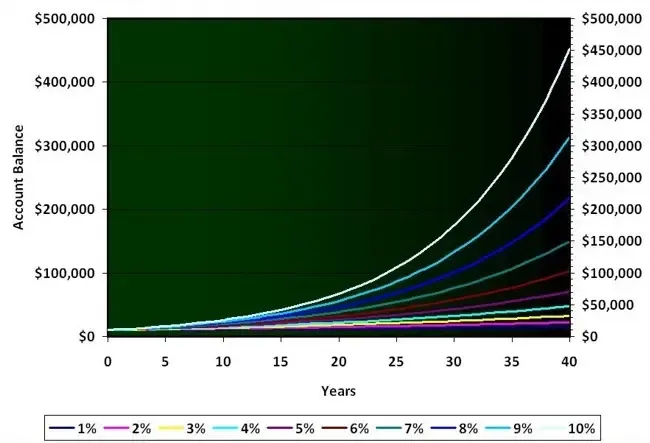

Historical data has shown us consistently that stocks outperform bonds in terms of returns over long periods of time (10 years +). The majority of retirement portfolios are not needed for at least 10 years. This is due to the fact that the majority of people are older than 10 years outside of retirement.

They’ll typically only begin to touch this money the day they retire. In the meantime, the idea is that our capital will grow as much as possible and give the greatest returns. Now if this is the case wouldn’t we want our portfolio composition to be aligned with the assets that the data shows historically give us the highest returns? Of course, there’s no way to predict the future, but certainly I want my portfolio to be evidence-based (just like my dentistry).

So why is it that the majority of these portfolios contain assets that inhibit their overall growth in value? Remember, the greater the rate of appreciation of our portfolio is the sooner we reach retirement after all. The answer is an interesting one, the composition of our portfolio in this regard is usually based on an “Attitude to Risk Assessment". This attitude to risk assessment attempts to quantify our attitude to risk (no surprises). We are assessed on a scale and put in a box based on our perceived attitude to risk. This is quantified from low to high.

A “higher risk” portfolio is said to be one that is more weighted towards stocks. A “lower risk” portfolio is said to be one more weighted towards bonds. Of course, what is said to be risk stems from our interpretation of the term risk. If both assets have the same amount of data to back up their longevity, and both have shown consistent appreciation over many decades, then can one be said to be truly more risky than the other in that sense?

Actually what they are equating risk to be is the VOLATILITY of the assets.

Volatility is the amount the price fluctuates over time. But as a general rule, the assets that have greater volatility also have greater returns (Not always of course – but in these cases they do). So with that said – shouldn’t we be looking for the assets with greater volatility? As these have scope to accelerate the date we can become financially free? And isn’t the greatest risk of all that the returns we achieve in a “low-risk” portfolio will never be enough for us to reach financial freedom?

FLIP the conventional interpretation of risk on its head and you’re closer to the mark in my opinion on this one.

The more you know.

Enter your details above to receive a link you can use to download your FREE pdf

Read More

Here's What New Associates Need To Know

What Is Your Definition Of Retirement?

How Often Do You Look Back On Your Life And Think “I Wish That I Knew Than What I Know Now?”

Can I Invest In My ISA For Passive Income?

The Role Of Luck In Investing

DENTISTS WHO INVEST LIMITED IS A LIMITED COMPANY, REGISTERED IN ENGLAND AND WALES